-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李浩然先生(Eric Li)

高級分析師

高級分析師

現任現為輝立証券持牌高級分析師,曾任職股票基金、家族辦公室及證券公司等,擁有多年的證券研究部門從業及投資經驗,並先後於香港最暢銷的財經媒體撰寫投資專欄。畢業於香港理工大學電子計算系。

Eric is currently a licensed research analyst at Phillip Securities. Prior to joining Phillip Securities, he has years of equity research and investment experiences in asset management company, family office and securities company. Meanwhile, he has written investment columns in Hong Kong`s best-selling financial media for years. He holds Bachelor of Arts in Computing from The Hong Kong Polytechnic University.

| Phone: | 22776516 | Email: | erichyli@phillip.com.hk | |

Yum China Holdings, Inc. (9987.HK) - 2Q2024FY revenue and operating profit hit 2Q record highs

Thursday, October 24, 2024  1192

1192

Yum China Holdings, Inc.(9987)

| Recommendation | Neutral |

| Price on Recommendation Date | $351.000 |

| Target Price | $337.000 |

Weekly Special - 601689 Tuopu Group

Yum China Holdings, Inc. (09987) is the largest restaurant company in China in terms of 2023 system sales, with 15,423 restaurants covering over 2,100 cities primarily in China as of June 30, 2024. Its growing restaurant network consists of our flagship KFC and Pizza Hut brands, as well as emerging brands such as Lavazza, Huang Ji Huang, Little Sheep and Taco Bell. The company has the exclusive right to operate and sublicense the KFC, Pizza Hut and Taco Bell brands in China (excluding Hong Kong, Macau and Taiwan), and own the intellectual property of the Little Sheep and Huang Ji Huang concepts outright. The company also established a joint venture with Lavazza Group, the world-renowned family-owned Italian coffee company, to explore and develop the Lavazza coffee concept in China.

2Q2024FY revenue and operating profit hit 2Q record highs

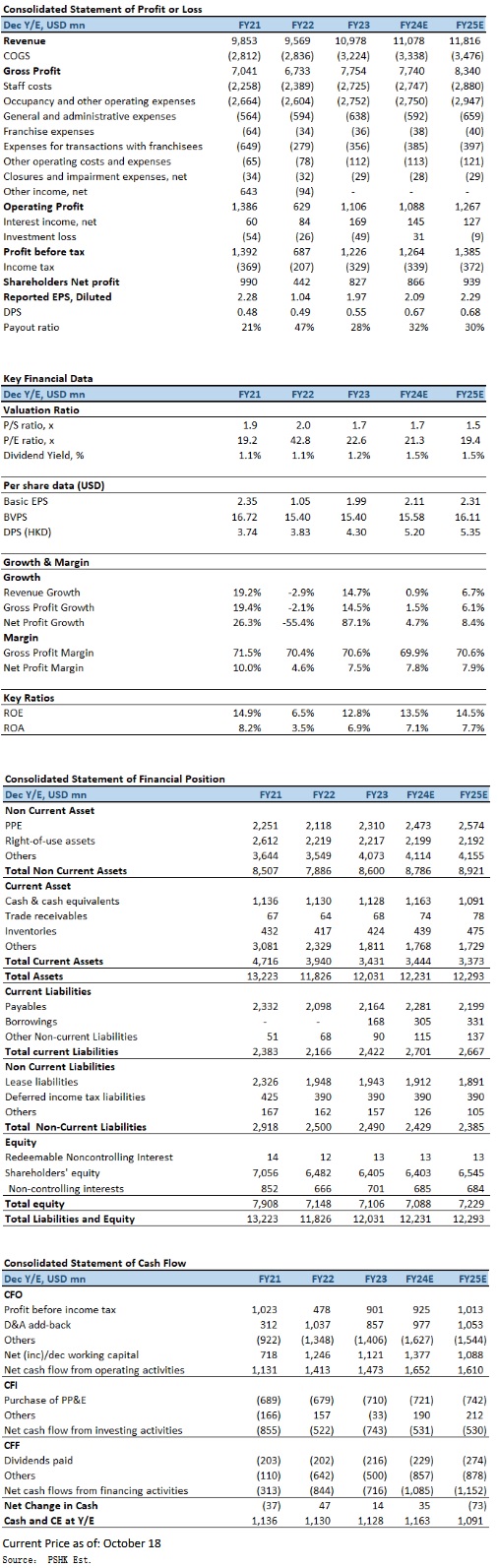

2Q2024FY, total system sales grew 4% YoY, excluding foreign currency translation ("F/X"), on top of last year's high base. The growth was primarily attributable to 8% of net new unit contribution. The Company opened 401 net new stores in the quarter. 99 net new stores, or 25%, were opened by franchisees. Total revenues increased 1% YoY to $2.68 billion, a record-high for the second quarter. Excluding F/X, total revenues would have been $85 million higher, or a 4% increase YoY. Same-store sales reached 96% of the prior year's level. Same-store transactions grew 4% YoY. Operating profit grew 4% YoY to $266 million, a record level for the second quarter. Excluding F/X, operating profit would have been $9 million higher, or a 7% increase YoY. Core operating profit grew 12% YoY to $275 million. OP Margin was 9.9%, an increase of 20 basis points YoY, supported by resilient restaurant margins and savings in G&A expenses. Restaurant margin was 15.5%. Excluding $12 million in items affecting comparability, restaurant margin was approximately the same as the second quarter last year. Improvement in operational efficiencies supported margin stability. Diluted EPS increased 17% YoY to $0.55, a record level for the second quarter, or up 19% YoY excluding F/X. Delivery sales grew 11% YoY, maintaining the double-digit growth Yum China has carried over the past decade. Delivery contributed ~38% of KFC and Pizza Hut's Company sales.

System sales for KFC grew 5% YoY for the Q2, on top of high base last year, primarily driven by net new unit contribution of 8%. KFC opened 328 net new stores during the quarter. 74 net new stores, or 23%, were opened by franchisees. Total store count reached 10,931 as of June 30, 2024. Operating profit was $264 million. Core operating profit was $273 million for the quarter, up 4% YoY. Restaurant margin was 16.2% for the quarter. Excluding items affecting comparability, restaurant margin decreased by 60 basis points against a strong comparison in the second quarter of 2023, primarily due to increased value-for-money offerings to drive traffic and wage inflation, partially offset by favorable commodity prices and improved operational efficiency. Delivery sales grew 12% YoY, contributing ~38% of KFC's Company sales for the quarter. Off-premises dining accounted for ~67% of KFC's Company sales.

System sales for Pizza Hut grew 1% YoY for the quarter, on top of high base last year, primarily driven by net new unit contribution of 8%. Pizza Hut opened 79 net new stores during the quarter. Total store count reached 3,504 as of June 30, 2024. Operating profit grew 13% YoY to $40 million, a record level for the second quarter. Core operating profit was $41 million, up 23% YoY. Restaurant margin was 13.2% for the quarter. Excluding items affecting comparability, restaurant margin was up 110 basis points YoY. Higher operational efficiency offset the impact of increased value-for-money offerings and wage inflation, resulting in an increased margin. Delivery sales grew 6%, contributing ~38% of Pizza Hut's Company sales for the quarter. Off-premises dining accounted for ~48% of Pizza Hut's Company sales.

Total revenues for the year to date ended June 30, 2024 increased 1%, or 5% excluding the impact of F/X. The increase in Total revenues excluding the impact of F/X, was driven by 8% net new unit contribution, partially offset by same-store sales decline, resulting from lower ticket average and same-store transaction growth. Same-store sales reached 97% of the prior year's level, against a strong performance in the same period last year. Operating profit decreased 5% YoY, or was almost flat with prior year excluding F/X. Savings in G&A partially offset the lower Restaurant margin, which was 16.6% year to date. Core operating profit grew 5% to $671 million. Diluted EPS increased 10% YoY to $1.26, or 14% excluding F/X. 1H2024FY, the Company returned a record $994 million to shareholders, including buying back 21.7 million shares of common stock, which is equivalent to over 5% of its outstanding shares as of December 31, 2023.

Full-year guidance remains unchanged

The Company's targets for the 2024 fiscal year remain unchanged from the prior period's disclosures. Open ~1,500 to 1,700 net new stores. Make capital expenditures in the range of approximately $700 million to $850 million. Return a Company record-setting $1.5 billion to shareholders through quarterly cash dividends and share repurchases.

Investment Thesis

The company achieved our most profitable second quarter since the spin-off, with core operating profit growing by 12% despite challenging industry dynamics. Total membership of KFC and Pizza Hut exceeded 495 million. Member sales accounted for over 65% of KFC and Pizza Hut's system sales in aggregate. KFC has successfully gained market share on delivery platforms by expanding its price range and lowering delivery fees. Pizza Hut attracted value-conscious customers with its entry-price pizzas and solo diners with its Pizza Dough Burger. Its business model breakthroughs enabled the company to broaden our addressable market and capture more customer occasions. With its industry-leading capabilities and scale, by reducing the complexity of menus and operations, and harnessing the power of automation and AI, the company improved operational efficiency, which help the company turning challenges into a greater competitive advantage in the context of a sluggish consumer market. We expect FY2024E-FY2025E EPS to be $2.11 and $2.31 respectively, with PT of HKD337.00, implies a FY2024E P/E of 20.5x (~1-yrs historical average + 1 standard deviation). Our investment rating is “Neutral”.

Risk factors

1) The price of raw materials continues to rise; 2) market competition intensifies; 3) Food safety risks; and 4) New store expansion falls short of expectations.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()